What Does An Underwriter Do In A Mortgage

Ever found yourself scrolling through Zillow, dreaming of that perfect little bungalow or sleek city apartment, only to hit a wall of mortgage jargon? You know, the stuff about approvals, rates, and underwriters? It’s enough to make anyone want to just rent forever. But fear not, future homeowners! Let's break down what exactly an underwriter does in the mortgage world, and why they're actually your unsung heroes.

Think of it like this: you’re embarking on a grand adventure to claim your own piece of the planet. The mortgage lender is like your trusty guide, but before they hand over the keys, they need to be absolutely sure you're up for the journey and that the treasure you're eyeing is as solid as it seems. That's where the underwriter steps in. They're the meticulous mapmakers and risk assessors of the whole operation.

So, what is an underwriter? In the simplest terms, they’re the decision-makers. They’re the ones who look at your mortgage application and all the accompanying documents and say, "Yes, this loan is a good idea for everyone involved," or, "Hmm, maybe we need to look a little closer here." It’s a role that requires a keen eye for detail and a solid understanding of risk. They’re essentially the gatekeepers of good loans.

The Underwriter's Mission: Risk Management (But Make It Chill)

At its core, mortgage underwriting is all about risk management. The lender is extending a significant amount of money, and they need to be confident they'll get it back. The underwriter’s job is to assess the likelihood of that happening. They look at a whole bunch of factors to build a complete picture of your financial health and the property itself.

Imagine you're making a really important investment, like buying a vintage record collection. You wouldn’t just grab the first box you see, right? You'd check the condition of the vinyl, the sleeves, maybe even listen to a few tracks. The underwriter does something similar, but with much bigger stakes.

It’s not about being stingy or making life difficult. It’s about ensuring the financial system stays healthy. If lenders were to hand out mortgages to just anyone without careful consideration, it could lead to widespread defaults, and nobody wants a rerun of the 2008 financial crisis, right? Underwriters are the unsung heroes preventing that kind of domino effect.

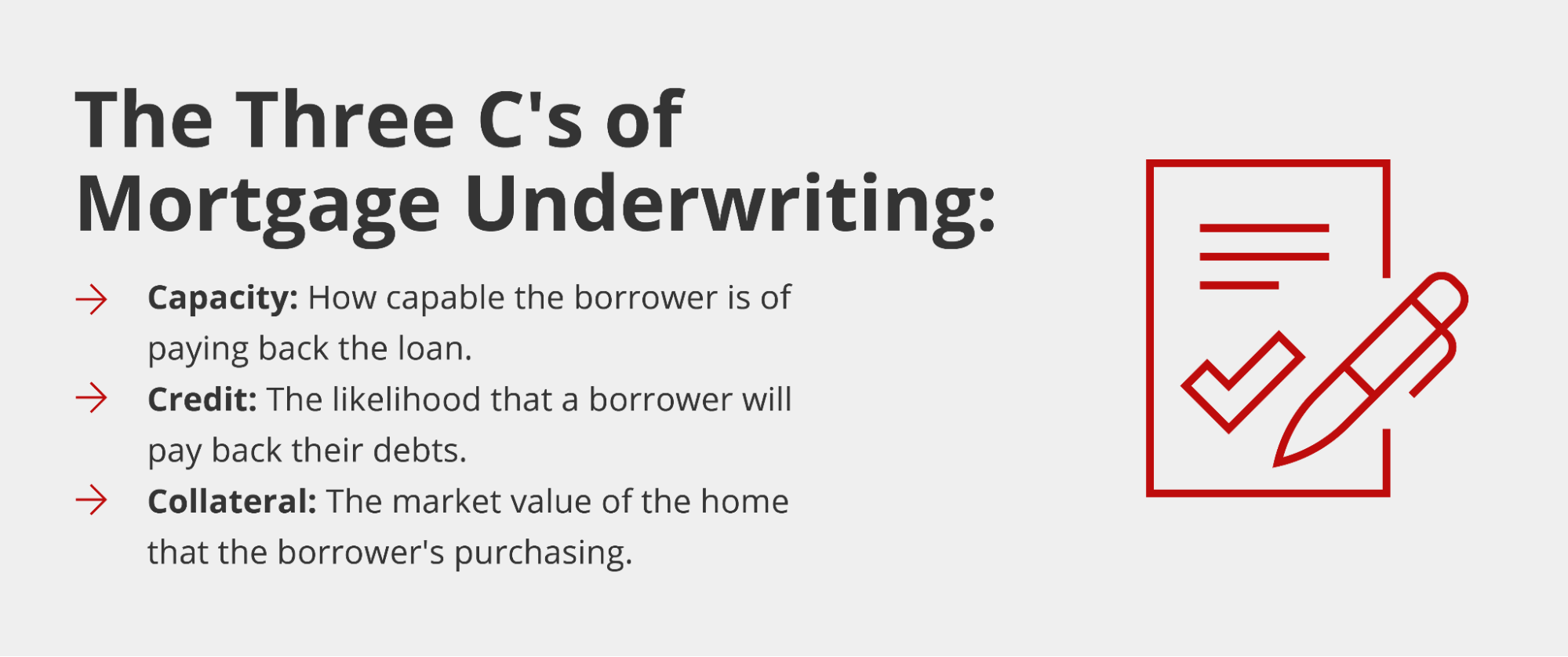

The Pillars of Underwriting: What They Scrutinize

So, what exactly does an underwriter pour over? Think of it as a three-legged stool, with each leg being crucial for stability:

1. Your Creditworthiness: The Financial Report Card

This is probably the most talked-about aspect. Your credit score is like your financial report card. A higher score generally means you’ve been responsible with borrowing and repaying money in the past. Underwriters will dig into your credit history to see:

- Payment History: Are your bills paid on time? Late payments are a red flag, like showing up late to your own surprise party.

- Credit Utilization: How much of your available credit are you using? Maxing out credit cards can signal financial strain. Think of it as not leaving enough room on your plate for dessert.

- Length of Credit History: A longer history of responsible credit use is generally viewed favorably. It shows a track record.

- Types of Credit: A mix of different credit types (credit cards, installment loans) can be a good sign.

- New Credit: Opening too many new accounts in a short period might raise eyebrows.

They’ll also look at your debt-to-income ratio (DTI). This compares your total monthly debt payments (including the potential new mortgage payment) to your gross monthly income. A lower DTI generally means you have more financial flexibility. Lenders have guidelines for acceptable DTI, and the underwriter ensures your application meets them. It’s like making sure your budget can handle the avocado toast habit and the mortgage.

2. Your Income and Employment Stability: The "Can You Afford This?" Check

Next up, the underwriter wants to know you have a steady and sufficient income to handle those monthly payments. This involves a deep dive into your employment and income sources:

- Employment Verification: They’ll confirm your job title, salary, and how long you’ve been with your employer. Job hopping too frequently can be a concern. They want to see some stability, not just a whirlwind romance with each job.

- Income Documentation: This means scrutinizing pay stubs, tax returns (usually the last two years), and sometimes bank statements. If you're self-employed, this can get a bit more involved, requiring detailed profit and loss statements and business tax returns. They need to be sure your income is real and sustainable, not just a hypothetical figure from your favorite sitcom.

- Other Income Sources: If you have rental income, alimony, or other sources of income, they'll want documentation for those too. It’s all about proving you have the cash flow.

This is where the underwriter plays a crucial role in preventing over-borrowing. They’re not just looking at your income today, but its likely trajectory. They want to ensure that a sudden job loss or a dip in business wouldn't leave you underwater (pun intended).

3. The Property Itself: The House as an Asset

It's not just about you; it's also about the asset you're buying. The underwriter will also assess the property to ensure it's a sound investment for both you and the lender:

- Appraisal: This is a professional assessment of the property's market value. The underwriter will review the appraisal report to make sure the loan amount doesn't exceed the property's worth. If the appraisal comes in low, it can be a deal-breaker, or lead to a need for a larger down payment. It’s like making sure the vintage watch you’re buying is actually worth what the seller is asking.

- Title Report: This report checks for any liens, easements, or other claims against the property that could affect ownership. The underwriter needs to ensure the title is clear, meaning you'll be the undisputed owner. Think of it as making sure nobody else has a claim to that primo parking spot.

- Property Type and Condition: In some cases, especially for unique properties or those with potential issues, the underwriter might want to see additional reports, like a pest inspection or survey. They want to make sure the house is structurally sound and doesn't come with any unwanted surprises, like a family of raccoons living in the attic.

The appraisal is particularly important. The lender wants to be sure that if, for any reason, they had to foreclose, they could sell the property and recover the loan amount. It's a crucial safeguard.

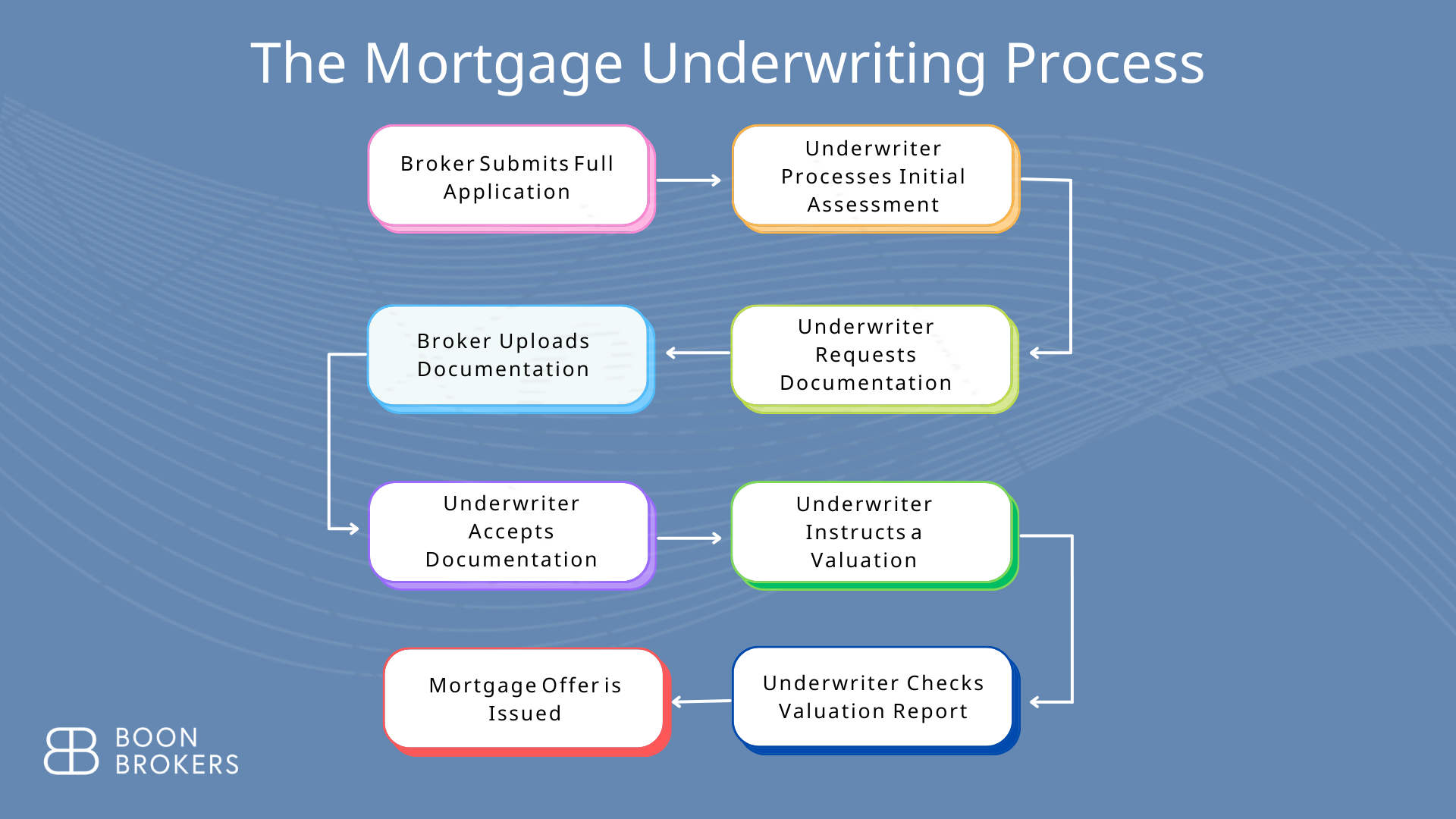

The Underwriting Process: Behind the Scenes

So, how does all this information come together? It's a process, and sometimes it can feel like a bit of a black box. Here's a simplified look at what happens:

First, you submit your mortgage application and all the supporting documents. Your loan officer or mortgage broker acts as your liaison, gathering everything and sending it to the underwriting department. This is where the real deep dive begins.

The underwriter will meticulously review every document. They’re looking for consistency, accuracy, and any potential red flags. They might ask for clarification on certain points or request additional documentation if something isn't clear. This is where patience becomes a virtue for the borrower!

They use sophisticated software systems to analyze your financial data and compare it against the lender's guidelines and sometimes even industry-wide standards. It's a blend of technology and human judgment.

Based on all the information, the underwriter makes a decision. This decision usually falls into one of three categories:

- Approve: Congratulations! The loan is approved, usually with specific conditions that need to be met before closing. These are often minor things, like providing a final pay stub or clarifying a transaction.

- Approve with Conditions: This is also a common outcome. The loan is approved, but only if certain requirements are met. Think of it as a conditional "yes."

- Deny: Unfortunately, sometimes the application doesn't meet the lender's criteria. The underwriter will provide a reason for the denial.

It’s important to remember that underwriters are human. They can make mistakes, and sometimes their interpretation of guidelines can be rigid. If you feel your application was unfairly denied, you can always ask for a reconsideration or seek advice from a mortgage professional.

The Underwriter's Toolkit and Skills

What makes a good underwriter? It's a combination of hard skills and soft skills. They need to be:

- Analytical: The ability to dissect complex financial data is paramount.

- Detail-Oriented: Missing even a small detail can have significant consequences. They’re like detectives, but for finances.

- Knowledgeable: They need a deep understanding of lending regulations, financial principles, and risk assessment.

- Ethical: Integrity is crucial, as they hold a position of significant responsibility.

- Good Communicators: They often need to explain complex decisions to loan officers and, indirectly, to borrowers.

Think of them as the guardians of responsible lending, ensuring that the system remains robust and fair. They are the unsung heroes who help millions achieve their dream of homeownership without jeopardizing their financial future or the stability of the market.

A Little Fun Fact: The Evolution of Underwriting

In the old days, underwriting was a much more manual and paper-intensive process. Imagine stacks of folders, meticulous calculations done by hand, and a lot more face-to-face interaction. Today, while human judgment is still vital, technology has revolutionized the process. Automated underwriting systems (AUS) can quickly analyze data and provide initial recommendations, freeing up human underwriters to focus on more complex cases and the nuances that technology might miss. It’s a bit like how streaming services changed the way we consume movies – the core is still there, but the delivery is vastly different and more efficient.

When Does an Underwriter Get Involved?

An underwriter typically gets involved after your initial application is submitted and reviewed by a loan officer or broker. Once the basic requirements seem to be met, the application is sent to the underwriting department for a thorough evaluation. They are involved right up until the point of loan approval, and sometimes even after, if any conditions need to be met before the final closing.

Common Reasons for Underwriter Concerns

What might raise an underwriter's eyebrows? Some common concerns include:

- Significant gaps in employment history.

- A large number of recent credit inquiries.

- High debt-to-income ratios.

- Unexplained large deposits or withdrawals in bank accounts.

- Appraisals that come in significantly below the purchase price.

- Discrepancies between information on the application and supporting documents.

Being prepared and having all your documentation in order can help mitigate these concerns. It’s like packing all your essentials for a road trip – the better prepared you are, the smoother the journey.

The Underwriter and You: Building Trust

While it might feel like the underwriter is this distant, mysterious figure scrutinizing your every financial move, remember their goal is ultimately to facilitate a sound loan. They are part of a system designed to protect both the borrower and the lender.

Think of them as the diligent librarian who carefully curates the collection, ensuring that every book (loan) is in good condition and will be returned. They’re not trying to stop you from borrowing the book; they just want to make sure you’re ready for it and that it’s a good fit for your needs and your ability to return it.

Being transparent, organized, and responsive to their requests can make the entire process smoother. They are, in essence, working to give you the green light for your financial future.

A Little Reflection

In our daily lives, we’re constantly making mini-underwriting decisions. When you decide whether to make that impulse purchase, you’re assessing your budget and future needs. When you choose to save a portion of your paycheck, you’re managing your financial risk. When you research a major purchase, you’re evaluating the "asset." The mortgage underwriter is simply doing this on a much larger, more formal scale. They’re the professionals who ensure that when you finally get the keys to your new home, it’s a decision that’s well-grounded, secure, and sets you up for a happy, stable future. And that, in the grand scheme of life’s adventures, is pretty darn important.