What Credit Rating Do I Need For A Mortgage

So, you're dreaming of your own little slice of the world, huh? That cozy home with the picket fence, or maybe a cool city loft with a killer view. Whatever your dream pad looks like, there's a pretty good chance you'll be needing a mortgage to make it happen. And when it comes to mortgages, there's this one little thing that pops up again and again: your credit score. It sounds a bit mysterious, right? Like a secret handshake into the world of homeownership.

But don't sweat it! We're going to break it down, nice and easy. Think of your credit score like your financial report card. It tells lenders how well you've handled borrowed money in the past. A higher score generally means you're seen as a lower risk, and that's a good thing when you're asking for a chunk of cash to buy a house.

What's This "Credit Score" Thing Anyway?

Basically, there are a few different credit bureaus that keep tabs on your financial habits. The most common scores you'll hear about are FICO and VantageScore. They take into account things like how often you pay bills on time, how much debt you currently have, how long you've had credit, and whether you've recently opened a bunch of new accounts.

Imagine your credit score as a superhero ranking. A score in the 300s? Well, that's like a villain who’s always late on their evil plans. A score in the high 700s or 800s? That’s your top-tier superhero, dependable and trustworthy. Lenders love those superheroes!

So, What's the Magic Number for a Mortgage?

Here's where it gets interesting. There isn't a single, rigid "magic number" that guarantees you a mortgage. It's more of a sliding scale, and it depends on the type of mortgage you're applying for and the specific lender. But generally speaking, you'll want to aim for a score that makes lenders feel comfortable.

For a conventional mortgage (the most common kind), a score of 620 or higher is often considered the minimum. However, getting approved with a score in this range might mean you're looking at higher interest rates and stricter terms. It’s like trying to get the best seat at a concert with a last-minute ticket – you might get in, but you might not have the ideal view.

If you're aiming for the best interest rates and most favorable loan terms, you'll want to shoot for a score in the 700s or even 800s. Think of this as getting front-row tickets. Lenders are much more eager to work with borrowers who have a strong credit history, and they'll reward you with lower monthly payments over the life of your loan. Over 30 years, that can add up to tens of thousands of dollars saved!

What About Those "Easier" Mortgages?

Now, what if your credit score isn't quite in the superhero stratosphere yet? Don't despair! There are government-backed loan programs designed to help more people become homeowners. These are often referred to as "government-insured" or "government-guaranteed" loans.

FHA loans, for example, are a popular option for borrowers with lower credit scores. You might be able to qualify for an FHA loan with a credit score as low as 500 if you have a substantial down payment (around 10%). If you have a credit score between 500 and 579, you'll typically need a down payment of at least 3.5%. These loans are fantastic because they open the door to homeownership for folks who might otherwise be shut out.

Then there are VA loans, available to eligible veterans, active-duty military personnel, and their surviving spouses. These loans are amazing because they often require no down payment and no private mortgage insurance (PMI), regardless of your credit score! While there isn't a strict minimum credit score set by the VA itself, most lenders will still have their own requirements, often around 580-620. Still, it's a seriously great perk!

And let's not forget USDA loans, for those looking to buy in eligible rural and suburban areas. These also often come with no down payment requirement, and credit score requirements can be more flexible, often around 640, though again, lenders might have their own benchmarks.

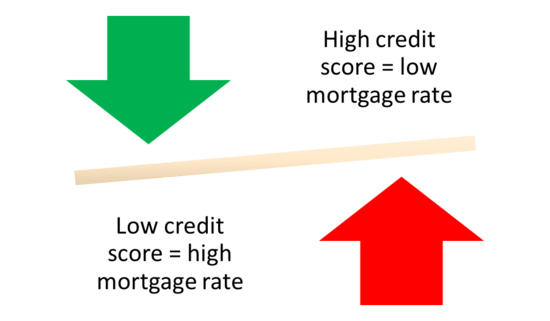

Why Does a Good Score Matter So Much?

It all boils down to risk. Lenders are in the business of lending money, but they also want to make sure they get that money back, with interest. A higher credit score signals to them that you're a responsible borrower who's likely to make your payments on time. It's like choosing a reliable car for a long road trip versus a car that might break down on you halfway there.

When your credit score is good, you get:

- Lower Interest Rates: This is the big one. Even a small difference in your interest rate can save you a fortune over the 30 years of a mortgage.

- Better Loan Terms: You might have more flexibility with repayment options or fewer fees.

- Larger Loan Amounts: Lenders might be willing to approve you for a bigger loan if they see you as a low-risk borrower.

- Easier Approval: The whole process can be smoother and less stressful.

So, What's the Verdict?

While a score of 620 is often seen as the baseline for conventional loans, aiming for 700+ will unlock the best deals. But don't get discouraged if you're not there yet. Government-backed loans like FHA, VA, and USDA offer fantastic alternatives for those with lower credit scores.

The key takeaway? Your credit score is important, but it's not the only factor. Lenders also look at your income, your employment history, your debt-to-income ratio, and the size of your down payment. It’s a holistic picture.

If your credit score needs a little TLC, don't panic! There are plenty of resources and strategies to help you improve it. Paying bills on time, reducing credit card balances, and avoiding opening too many new accounts at once can all make a big difference. It might take a little time and effort, but the payoff – owning your dream home – is absolutely worth it!

So, go ahead, start dreaming, start planning, and definitely start paying attention to that credit score. It’s one of your biggest allies in the journey to homeownership!