Does Buy Now Pay Later Affect Credit Score

Let's dive into something that's become as common as scrolling through your favorite online store: Buy Now, Pay Later (BNPL). It's like a little financial magic trick, letting you snag that must-have item today and spread the cost over a few weeks or months. But here's the juicy part: does this convenient payment method play nice with your credit score? It's a question on a lot of minds, and understanding the answer can be super useful for keeping your financial health in tip-top shape.

Think of BNPL as a temporary loan, a way to bridge the gap between wanting something and actually paying for it. The purpose is simple: to make purchases more accessible and manageable, especially for larger items or when you want to avoid tying up all your cash at once. The benefits are pretty clear. For starters, it can help you budget better. Instead of a big hit to your bank account, you have smaller, predictable payments. This can be a lifesaver for unexpected expenses or when you're saving for a bigger goal. Plus, many BNPL providers offer interest-free installments if you pay on time, which is a fantastic way to save money compared to traditional credit cards with high interest rates. It's like getting a discount, but the retailer still gets paid upfront!

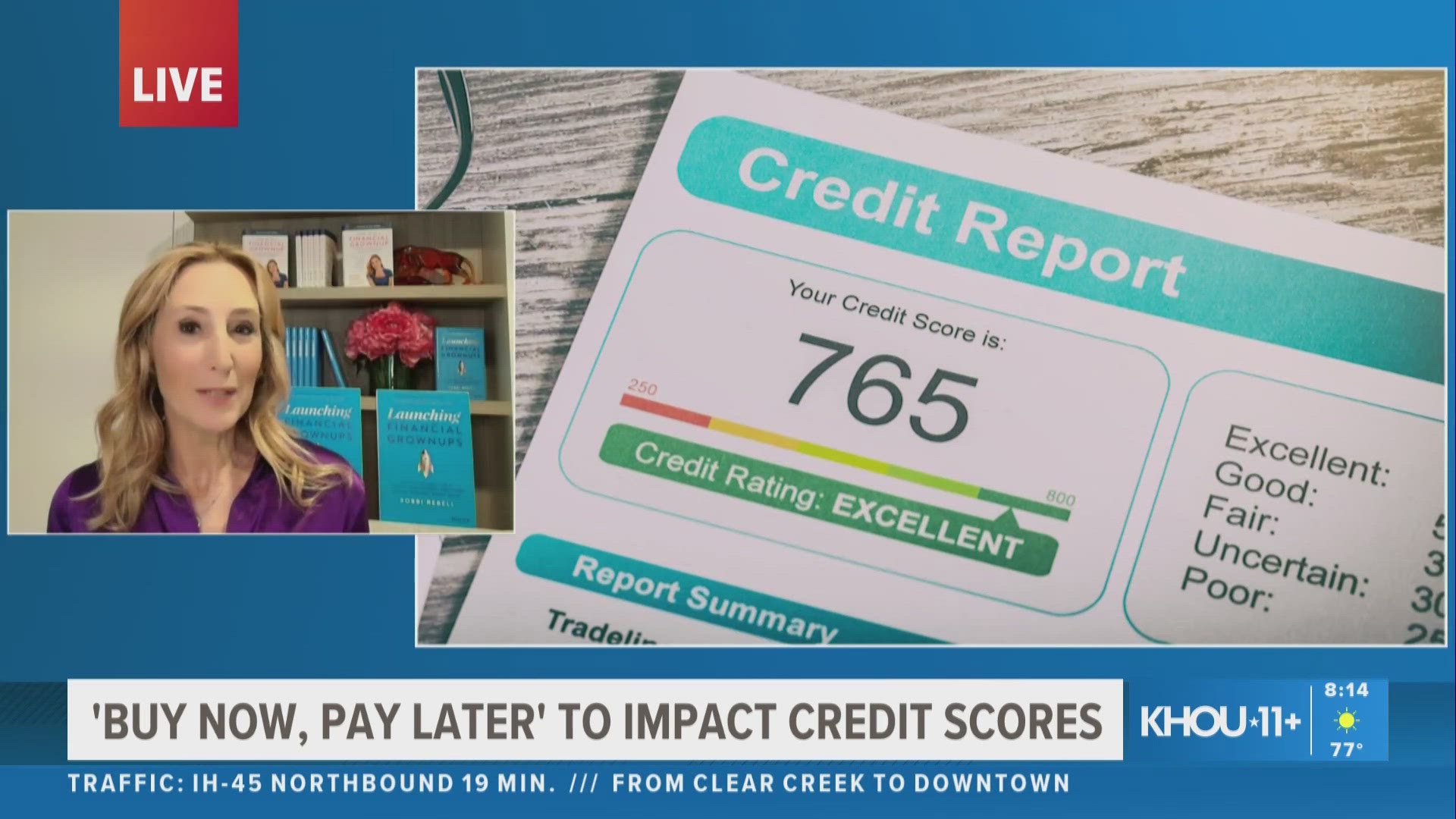

Now, about that credit score. This is where things get a little nuanced, and it's not a simple yes or no answer. Historically, many of the popular BNPL services, especially those that are paid off quickly (like the 4-payment options you see everywhere), didn't typically report to the major credit bureaus. This meant that using them, and even paying them off diligently, wouldn't directly impact your credit score in the same way a credit card or loan would. It was kind of a "what happens in BNPL, stays in BNPL" situation for your credit file.

However, the financial landscape is always evolving, and the BNPL world is no exception. As these services have exploded in popularity, credit bureaus and lenders have started to pay more attention. So, the answer to whether BNPL affects your credit score is increasingly becoming "it depends". Here's why:

- Reporting Practices Vary: Not all BNPL providers are created equal when it comes to reporting. Some do now report your payment activity to credit bureaus like Experian, Equifax, and TransUnion. This means that your on-time payments could potentially help build a positive credit history, but late payments could definitely hurt it. Other providers might only report if you fall significantly behind or default on your payments. It's crucial to check the specific terms and conditions of the BNPL service you're using to understand their reporting policies.

- "Soft" vs. "Hard" Inquiries: When you apply for a BNPL plan, it typically involves a "soft inquiry". This is like a quick look at your creditworthiness that doesn't affect your score. Think of it as them peeking at your credit report without taking a deep dive. This is different from a "hard inquiry," which happens when you apply for a credit card or loan and can have a small, temporary impact on your score. Most BNPL providers stick to soft inquiries for their initial checks.

- Potential for Debt Accumulation: While BNPL might seem like "free money," it's still a form of debt. If you're juggling multiple BNPL plans simultaneously, it can become easy to lose track of your payment deadlines. Falling behind on even one of these can have negative consequences, especially if that provider reports to the credit bureaus. Overspending and accumulating too much BNPL debt could also indirectly impact your creditworthiness if it strains your overall budget and leads to missed payments on other financial obligations.

- Impact on Credit Utilization (Indirectly): While BNPL payments themselves don't usually show up as a line item affecting your credit utilization ratio (which is the amount of credit you're using compared to your total available credit), the debt you accrue can still play a role in your overall financial health. If you're relying heavily on BNPL for everyday purchases, it might mean you have less disposable income to pay down other debts, potentially impacting your credit utilization on credit cards.

So, what's the takeaway here? BNPL can be a fantastic tool for managing your finances and making purchases more affordable, but it's not entirely invisible to the credit world anymore. The key is to be responsible and aware. Always know which providers report to credit bureaus and treat your BNPL payments with the same seriousness as you would any other bill. If you're consistently paying on time, it can be a neutral or even positive factor in your financial journey. However, if you’re prone to overspending or forgetting due dates, BNPL could become a tricky pitfall.

Here’s a good rule of thumb: always read the fine print. Understand what the BNPL provider's policies are regarding credit reporting. If a provider does report, using it responsibly and making all your payments on time can be a way to gradually build a good credit history, especially for those who are new to credit or looking to improve their scores. Conversely, late payments or defaults can certainly leave a negative mark. It’s a bit like having an extra, albeit sometimes silent, player on your financial team. You want to make sure you’re playing the game right!

Ultimately, BNPL is a tool, and like any tool, it can be used effectively or ineffectively. By staying informed and making smart choices, you can enjoy the convenience of Buy Now, Pay Later without jeopardizing your hard-earned credit score. It’s all about being a savvy shopper and a responsible borrower!