Consumer Debt Stats: Are Americans Borrowing More As Growth Slows?

Hey there, friend! Let's dive into something that might sound a little dry but is actually pretty darn interesting: consumer debt stats. You know, that whole "are Americans borrowing more as growth slows?" question. Sounds like something your accountant might ramble on about, right? Well, fear not! We're going to break it down like a perfectly baked cookie – easy, enjoyable, and with a few sprinkles of fun thrown in.

So, what's the deal? Is everyone suddenly maxing out their credit cards because the economy is doing a bit of a "meh" dance? Or are we all just a little more… enthusiastic about putting things on the tab?

The Big Picture: Is the Wallet Getting Thicker or Thinner?

Let's start with the headline. Are Americans borrowing more? The short answer is, well, yes, by and large. When we talk about consumer debt, we're usually looking at things like credit card balances, auto loans, student loans, and personal loans. Think of it as the financial soundtrack to our everyday lives. And right now, that soundtrack seems to be getting a bit louder.

But here's the twist: is it because growth is slowing? That's the million-dollar question, isn't it? Sometimes, when the economy is humming along nicely, people feel confident and are more likely to take on debt to finance big purchases – a new car, a fancy vacation, you name it. When growth slows, you might expect folks to tighten their belts, right? Cut back on the lattes, maybe wear those shoes a little longer.

However, the data is a bit more nuanced. It's not always a simple "slow growth equals less borrowing" equation. Life happens, and sometimes borrowing becomes a necessity, not just a splurge. Think of it like this: if your income isn't keeping pace with rising prices, you might find yourself needing to borrow to cover the difference. It's not ideal, but it's a reality for many.

Credit Card Ballet: A Delicate Dance

Let's talk credit cards. They’re the flashy dancers in the consumer debt ballroom. And right now, they’re definitely doing a few more pirouettes than usual. We're seeing credit card balances tick up. It’s not a national emergency, but it’s definitely something to keep an eye on.

Why the increase? Well, a few reasons are often cited. First, inflation. Remember when a gallon of milk cost less than a fancy coffee? Good times. Inflation means that the same stuff you used to buy now costs more. So, even if your spending habits haven't changed much, your credit card bill will naturally go up. It’s like your wallet is trying to play catch-up, and sometimes it needs a little help from plastic.

Second, there's the ever-present allure of convenience. Credit cards are easy! Click, swipe, done. And let's be honest, sometimes you just need that new appliance, or you have an unexpected car repair, and putting it on the card feels like the most sensible option at the moment.

Now, are these rising balances a sign of distress? Not necessarily for everyone. Some people manage their credit cards like financial ninjas, paying them off diligently each month. For them, a higher balance might just reflect a temporary bump in spending or a strategic use of rewards programs (gotta get those travel miles, right?). But for others, it could be a sign that they're relying on credit to bridge the gap between income and expenses, which can become a bit of a slippery slope.

Auto Loans: Cruising into More Debt

Next up, the humble auto loan. For many, a car isn't a luxury; it's a necessity. It's how you get to work, ferry the kids, and maybe even escape to the mountains for a weekend. And lately, buying a car has gotten… expensive. Like, really expensive. So, it's no surprise that auto loan balances are also on the rise.

Think about it: car prices have shot up. Supply chain issues, increased demand – it all adds up to sticker shock at the dealership. If you need a new set of wheels and your old one has finally decided to retire (perhaps to a farm upstate), you might find yourself taking out a bigger loan than you anticipated. It’s less about wanting a fancy sports car and more about needing reliable transportation to keep your life moving.

The length of these loans is also stretching out. It used to be that a five-year loan was pretty standard. Now, it's not uncommon to see six or even seven-year terms. This means you're borrowing for longer, and while your monthly payments might be more manageable, you'll likely end up paying more in interest over time. It's a trade-off, for sure.

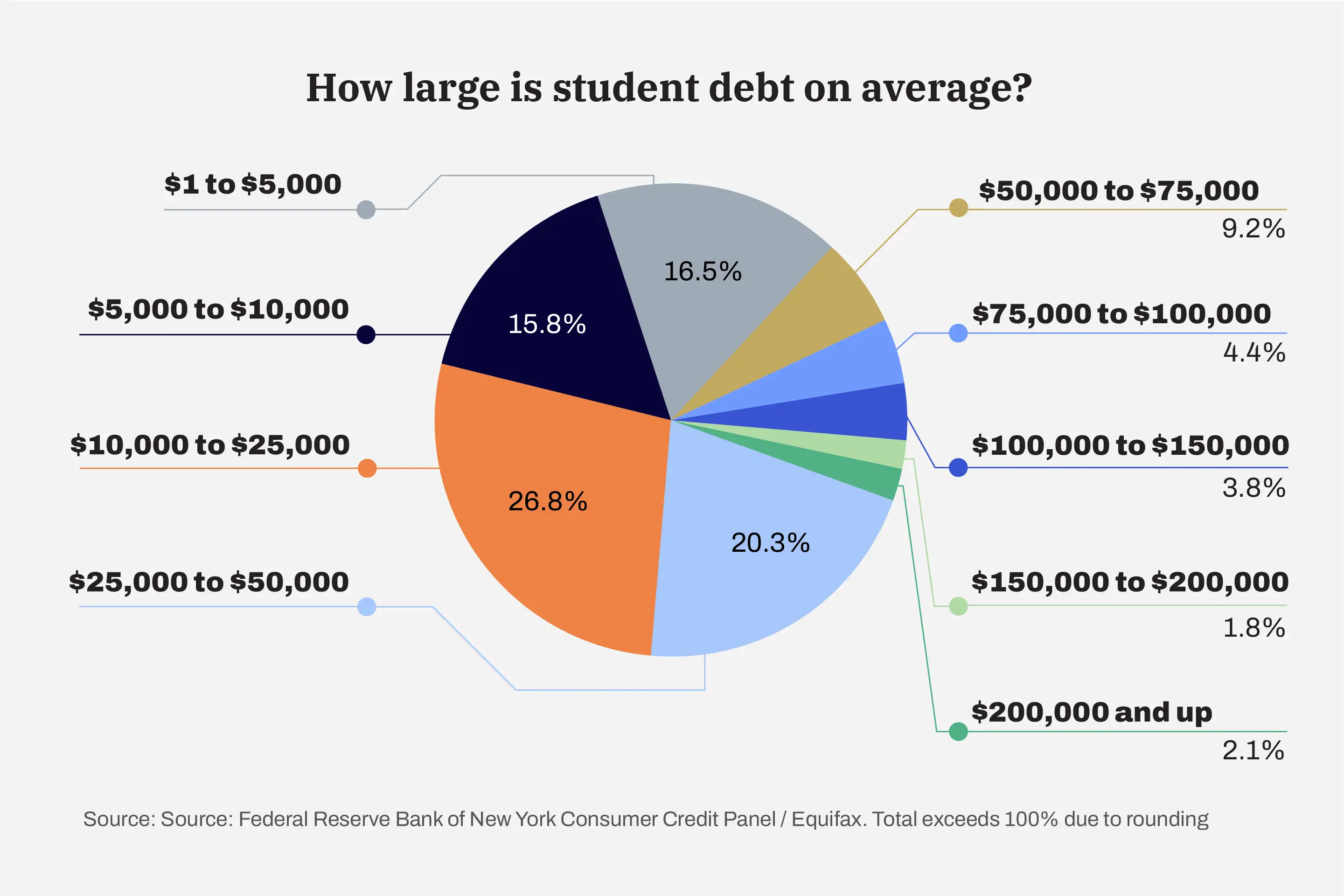

Student Loans: The Persistent Echo

Ah, student loans. This is a whole chapter in the book of American debt, and it’s a long one. For years, the cost of higher education has been climbing, and with it, the amount of money young people borrow to get their degrees. So, naturally, student loan debt remains a significant chunk of the overall consumer debt pie.

While there have been some governmental efforts to address this, the sheer volume of outstanding student loan debt is undeniable. It’s a persistent echo in many households, impacting financial decisions for decades. It’s not exactly a new trend, but it’s definitely a major contributor to the overall borrowing picture.

Is it directly linked to *slowing growth? It’s more of a parallel track. People still need and want education, and the cost remains high. So, borrowing continues, regardless of the immediate economic climate. It’s a long-term investment, or at least, that’s the hope!

The "Why" Behind the Borrowing Boom

So, let's get back to that "why." If growth is slowing, why are we seeing more borrowing in some areas?

Inflation: We mentioned this, but it bears repeating. When your paycheck doesn't stretch as far, you have a few options: cut back, earn more, or borrow. For many, borrowing becomes the most accessible, albeit temporary, solution.

Unforeseen Expenses: Life has a funny way of throwing curveballs. A medical emergency, a job loss, a major home repair – these things don’t care if the economy is booming or busting. And when they happen, borrowing is often the quickest way to get back on your feet.

Shifting Consumer Behavior: Sometimes, it's just about what we've come to expect. We're accustomed to a certain lifestyle, and when it becomes harder to afford it outright, we might rely on credit more readily. It’s a subtle shift, but it can add up.

Interest Rates: While interest rates have been on the rise lately, for a long time, they were historically low. This made borrowing cheaper and more attractive. Even with recent hikes, the relative cost of borrowing might still feel manageable for some, especially compared to the alternative of delaying necessary purchases.

Are We All Underwater? Not Necessarily!

Now, I don't want you to leave this conversation feeling like everyone is drowning in debt and the economy is about to do a dramatic nose-dive. That’s definitely not the whole story!

Here’s the good news: many Americans are still managing their debt responsibly. Credit scores are, in general, holding up reasonably well. Banks and lenders are also a bit more cautious than they were in the lead-up to the 2008 financial crisis. So, it’s not quite the Wild West out there.

Also, remember that not all debt is created equal. Mortgages, for example, are a form of debt, but they’re often seen as an investment in an asset. The debt we're primarily discussing here are the shorter-term, often higher-interest debts that consumers rack up for everyday expenses and purchases.

The key takeaway is that the increase in consumer borrowing, particularly in credit cards and auto loans, is a complex picture. It's influenced by inflation, unexpected life events, and evolving consumer habits, and it's happening in a period where economic growth is showing some signs of slowing. It’s a bit like a delicate balancing act – juggling rising costs with the desire to maintain a certain quality of life.

Looking Ahead: A Dose of Optimism

So, are Americans borrowing more as growth slows? The data suggests a trend towards increased borrowing in certain categories, often driven by necessity rather than pure indulgence. It’s a sign of the times, a reflection of economic pressures and the persistent need to keep life moving forward.

But here's the really important part, the part that should leave you with a little spring in your step: understanding these trends is the first step towards making smarter financial decisions for yourself. Whether it's about managing your credit card balances, planning for larger purchases, or thinking about long-term financial goals, knowledge is power!

And honestly, the resilience of people is pretty amazing. We navigate these economic bumps with ingenuity and determination. We find ways to stretch our dollars, to cut back where we can, and to plan for a brighter future. So, while the numbers might show an increase in borrowing, remember that they also represent people trying their best to live their lives, to provide for their families, and to achieve their dreams. And that, my friend, is a story worth smiling about.