Can You Get A Mortgage Without Life Insurance

Hey there, homebuyer extraordinaire! So, you're diving headfirst into the exciting, sometimes bewildering, world of mortgages. Congrats! It's like unlocking a new level in adulting, right? You've probably got a million questions buzzing around your brain, and one that might have popped up is: "Can I actually snag this dream home without signing up for life insurance?"

Let's get this straight, right off the bat. The short answer is... mostly, yes! It's not usually a hard and fast rule like, "No life insurance, no house key." Phew, right? Imagine the stress if it were! You'd be juggling mortgage applications and life insurance policies like a circus performer who's had too much coffee.

But, like most things in life (and especially in finance), there's a little bit of a "it depends" attached to it. Think of it like asking if you can bring your pet unicorn to the party. Usually not, but if the host loves unicorns and has a massive backyard, maybe!

The Lender's Perspective: Why They Might Nudge You Towards Life Insurance

So, why do some lenders even suggest life insurance when you're getting a mortgage? It's not because they're secretly plotting to make you buy more policies. Nope, it's all about risk management, baby! They've got a lot of money tied up in your mortgage, and they want to make sure they get their money back, no matter what.

Think of your mortgage as a really, really big loan. And lenders are, well, lenders. They're not in the business of wishing for the worst, but they do plan for it. If something unfortunate were to happen to you, the primary earner, who would pay the mortgage? That's where life insurance swoops in, like a superhero in a beige suit.

A life insurance payout could cover the outstanding mortgage balance, protecting both your family from losing their home and the lender from a potentially sticky situation. It's like a financial safety net. And lenders, bless their cautious hearts, love a good safety net.

Mandatory vs. Recommended: The Crucial Difference

Now, here's where it gets interesting. In most places, especially for your standard mortgage, life insurance is not a mandatory requirement to get approved. You can absolutely get a mortgage without it. High fives all around!

However, some lenders might strongly recommend it. They might even offer you a slightly better interest rate or a few perks if you do have it. It's their way of saying, "Hey, we appreciate you thinking ahead, and here's a little something for your troubles." It's not blackmail, it's just good business.

The only time it might become a harder requirement is in very specific situations, like if you have a particularly large loan, a less-than-stellar credit history, or if the lender has other concerns about your ability to repay. They might see life insurance as an extra layer of security that eases their worries. It's their way of sleeping better at night, and by extension, you might too!

What About Mortgage Protection Insurance (MPI)?

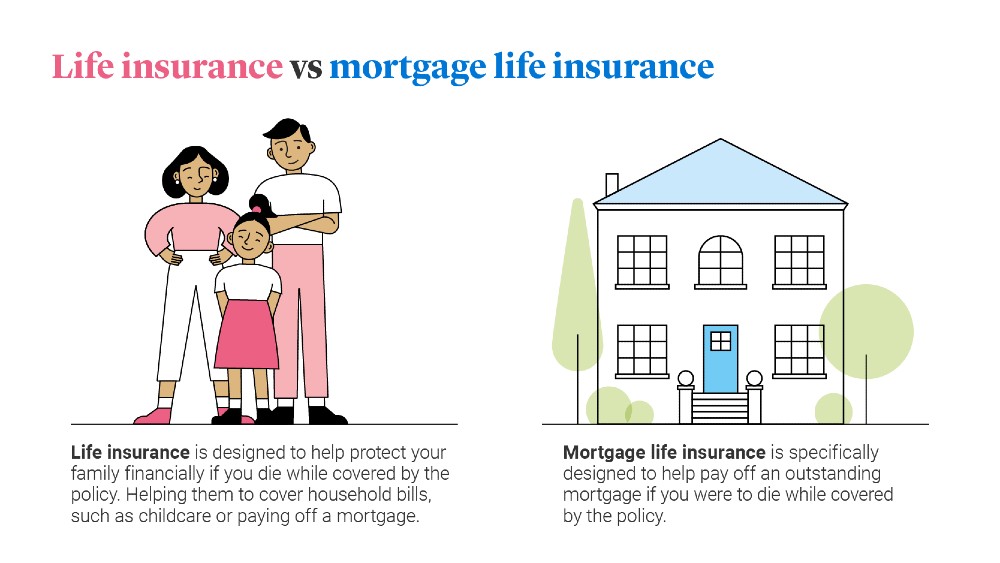

Ah, the sneaky cousin of life insurance! You might hear about something called Mortgage Protection Insurance (MPI). This is often offered by lenders, and it sounds perfectly tailored for your mortgage. It's designed to pay off your mortgage if you die, become disabled, or lose your job.

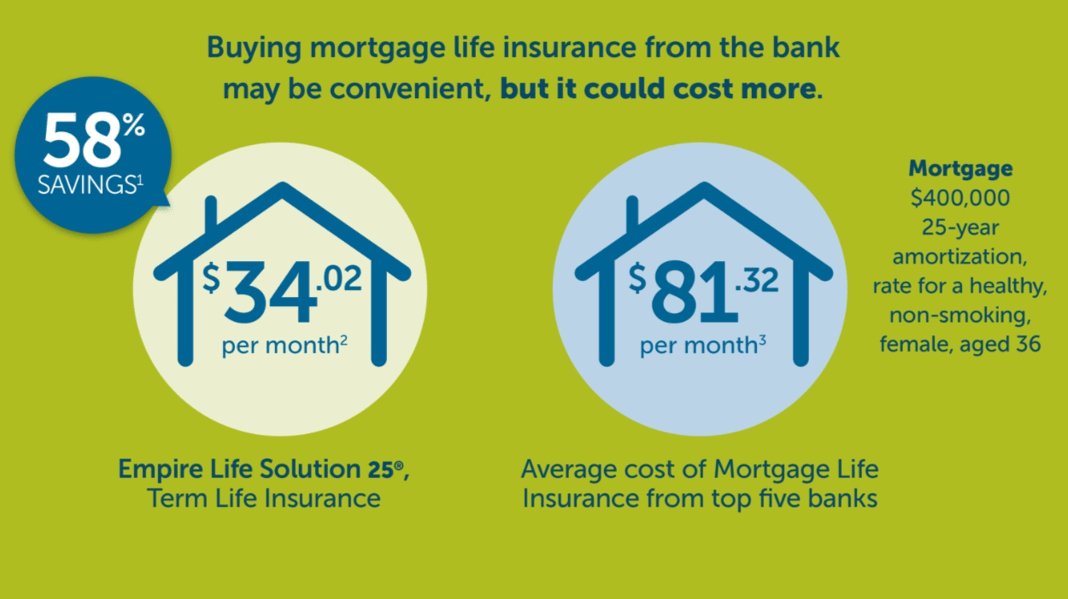

Sounds great, right? But here's the catch: MPI is often more expensive than a traditional term life insurance policy. And the benefits can be a bit less flexible. With term life insurance, the payout is a lump sum that your beneficiaries can use for anything – including paying off the mortgage, covering daily expenses, or even buying that alpaca farm you've always dreamed of.

MPI, on the other hand, usually pays the lender directly and the coverage amount decreases as you pay down your mortgage. It's like paying for a full steak dinner but only getting to eat half of it. So, while it can cover your mortgage, it's usually not the most bang for your buck compared to a standalone life insurance policy.

Think of it this way: If you're buying a really comfy couch, would you rather buy it from the furniture store that also sells throw pillows, or from a store that only sells throw pillows that are specifically shaped to fit that one couch? You get the idea!

Who Really Needs Life Insurance with a Mortgage?

So, if it's not mandatory, who should be scrambling to get a life insurance policy? Well, let's break it down:

You Have Dependents: The Big One!

This is the most obvious, and honestly, the most important reason. If you have a partner, children, or anyone else who relies on your income to keep a roof over their heads (and food on the table!), then life insurance is a no-brainer. Your mortgage is probably one of your biggest debts, and if you're gone, who's going to pick up that tab?

Imagine your kids graduating, or your spouse maintaining their lifestyle, without the looming shadow of a massive mortgage payment. That's peace of mind, my friends. It’s not about morbid thoughts; it's about protecting the ones you love the most.

You're the Sole Earner: Double the Responsibility

If you're the only one bringing home the bacon in your household, and you have a mortgage, life insurance becomes even more critical. Your income is the engine that powers the mortgage payments. Without it, the whole system grinds to a halt. It's like taking the batteries out of your remote control – suddenly, everything stops working!

You Have Other Significant Debts: Beyond the Mortgage

While the mortgage is a big one, if you also have other substantial debts like car loans, student loans, or business loans, life insurance can provide a safety net to cover those too. It's about ensuring your passing doesn't leave a financial disaster for your loved ones.

You Want to Leave a Legacy: More Than Just a House

Some people see life insurance as a way to leave a financial legacy. Beyond just covering debts, it can provide a cushion for your family to pursue their dreams, start a business, or simply live comfortably. It’s a gift that keeps on giving, even after you’re gone.

What if You Don't Have Life Insurance?

Okay, so let's say you're single, debt-free except for your (future) mortgage, and you're totally financially independent. Or maybe your spouse has a fantastic income that can easily cover everything. In these scenarios, life insurance might not be a top priority specifically for the mortgage.

You can still get a mortgage! The lender will still assess your financial situation, your credit score, your income, and your assets to ensure you're a good candidate. If you can prove you have the financial stability to make those payments, they'll likely approve you, life insurance or not. It's like showing up to a potluck with an amazing homemade dish – you're still welcome, even if you didn't bring the fancy napkins.

However, even if it's not required for the mortgage, it's still worth considering the general benefits of life insurance for your overall financial planning. Think of it as an investment in your loved ones' future security.

Tips for Navigating the Life Insurance Conversation

If your lender is pushing for life insurance, or if you're just curious about it, here are a few friendly tips:

- Ask Why: Don't be afraid to ask your lender why they're suggesting it. Understanding their reasoning can help you make a more informed decision.

- Shop Around: If you decide you do want life insurance, don't just go with the first option your lender throws at you. Compare quotes from different insurance companies. You might be surprised at the savings!

- Understand the Terms: Whether it's MPI or term life, make sure you understand the policy's terms, coverage, duration, and cost. No one likes nasty surprises, especially when it comes to finances.

- Consider Term Life: For most people, especially when it's tied to a mortgage, term life insurance is the most cost-effective option. It covers you for a specific period (the term) and is generally much cheaper than whole life insurance.

- Consult a Financial Advisor: If you're feeling overwhelmed, a good financial advisor can help you assess your needs and find the right insurance solutions. They're like your financial GPS!

The Big Picture: Owning a Home is Awesome!

So, can you get a mortgage without life insurance? Absolutely, in most cases! Don't let the thought of life insurance policies stand between you and your dream home. Focus on getting your finances in order, getting pre-approved, and finding that perfect place.

Life insurance is a fantastic tool for financial planning and protecting your loved ones. It's wise to consider it, especially if you have dependents or significant financial responsibilities. But if it's not a deal-breaker for your mortgage approval, don't sweat it too much. You've got this!

The journey to homeownership is a big accomplishment. Take a deep breath, enjoy the process, and remember that you're building a future for yourself, one step (and one mortgage payment!) at a time. And hey, if you end up getting that mortgage and a life insurance policy, you're just that much more of a financial superhero. You've got a safe, secure place to call your own, and the knowledge that your loved ones are protected. Now go forth and be awesome!