Best Way To Finance A Car For Self-employed

Remember Sarah? She’s the freelance graphic designer who practically lives in her car, zipping from client meetings to coffee shop workspaces. Last year, her trusty, slightly-too-old hatchback finally gave up the ghost. She was stuck, literally and figuratively. Getting to clients became a logistical nightmare, and honestly, a car that sputters more than it accelerates doesn’t exactly scream “professionalism.” She’d been putting off buying a new one, mostly because the thought of car financing as a self-employed individual felt… well, complicated. Like trying to explain to your grandma what SEO is. You know? She finally marched into a dealership, armed with a brave face and a whole lot of nervous energy.

And that’s where we are today. Because Sarah’s situation isn't unique. If you're out there building your own empire, working for yourself, and the idea of financing a car makes you break out in a cold sweat, you’re in the right place. Let’s ditch the jargon and talk real talk about how to get yourself some sweet new wheels without losing your mind (or your business). This isn’t your typical snooze-fest car loan article, I promise.

So, You're Self-Employed and Need a Car? Let's Not Make it a Drama.

Being self-employed is awesome, right? You’re your own boss, you set your own hours (mostly!), and you get to wear sweatpants to meetings if you’re feeling bold. But when it comes to big purchases like a car, it can feel like you’re on a different planet compared to your W-2-earning pals. They just flash a few pay stubs and boom, car keys. You? It’s more like a treasure hunt for documentation.

The good news is, it’s totally doable. You just need to approach it a little differently. Think of it as a strategic mission, not an impossible quest. We’re going to break down the best ways to finance that essential ride, so you can keep your business rolling and your commute… well, less embarrassing than Sarah’s old hatchback.

Why is it Different for Us Freelancers?

Alright, let’s get this out of the way. Lenders love predictability. Your traditional employer provides a consistent, verifiable income. For them, that’s a big fat green light. Your income, on the other hand, might have more peaks and valleys. One month you’re swimming in client work, the next… crickets. This variability can make lenders a bit… hesitant. They’re not trying to be mean; they’re just trying to manage their risk. It’s like when you’re trying to explain to your parents why you need that fancy new espresso machine for your home office. They just don’t get the ROI!

But fear not! Understanding this difference is the first step to overcoming it. We just need to present our financial picture in a way that makes sense and builds trust. Think of it as a persuasive presentation, not just a loan application.

Your Financial Game Plan: What Lenders Want to See

This is where you get to shine. You’re resourceful, you’re adaptable, and you’re probably pretty good at juggling a million things. This is just another one of those things. You need to show them you’re a stable and reliable borrower, even if your income doesn’t look like a straight line on a graph.

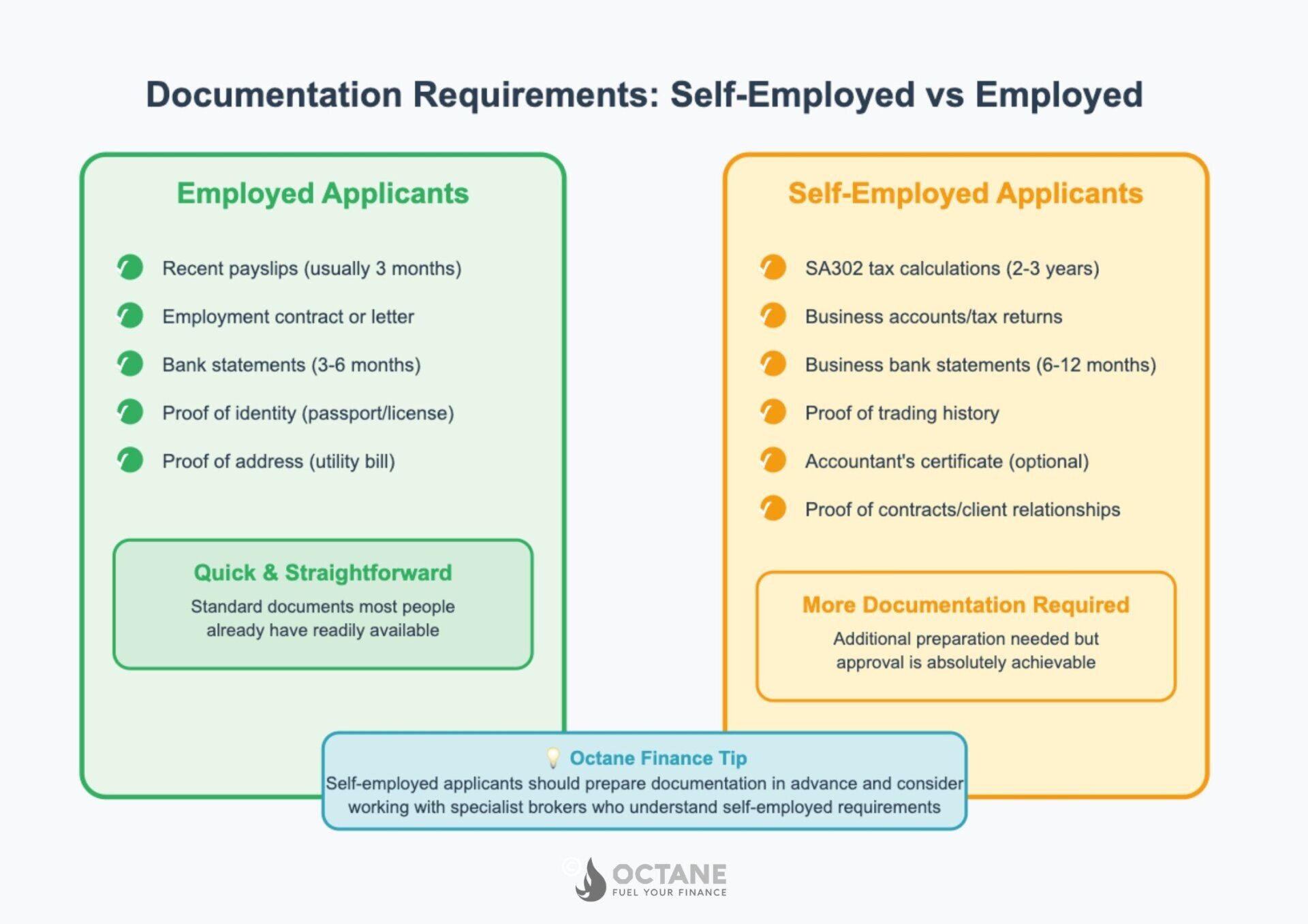

1. The Holy Grail: Your Documentation

This is probably the most important part. Get your ducks in a row. I mean, really get them in a row. Don’t just shove papers into a folder and hope for the best.

- Tax Returns: This is your golden ticket. Lenders will want to see at least two years of your most recent tax returns. This shows them your average income over time. Make sure you’re filing them accurately and on time! No scrambling at the last minute, okay?

- Profit and Loss (P&L) Statements: If you’re a more established business, a P&L statement that you prepare yourself (or with your accountant) can be incredibly valuable. It’s a snapshot of your business's financial performance over a period.

- Bank Statements: Again, have a good chunk of these ready – at least six months, maybe even a year. They show the actual cash flow coming into your business (and personal accounts). Look for consistency and healthy balances.

- Invoices and Contracts: Having signed contracts with clients and a list of outstanding invoices can demonstrate future income. This is especially powerful if you have long-term contracts. It’s like saying, “See? I’ve got work lined up!”

- Business License and Registration: Proof that your business is legitimate.

Seriously, folks, the more organized you are with this stuff, the smoother the process will be. Imagine a lender looking at your meticulously organized paperwork and thinking, “Wow, this person is on top of their game. They’re probably great at paying back loans too!”

2. Credit Score: Your Financial Report Card

Your credit score is your best friend, or… well, it’s not. If it’s not looking great, this is the time to put in some effort. A good credit score signals to lenders that you’re responsible with borrowed money. Pay your bills on time, reduce your credit card balances, and avoid opening too many new accounts right before applying for a car loan.

Think of it this way: if your credit score is a shaky foundation, adding the weight of a car loan is like building a skyscraper on quicksand. Not ideal.

3. Down Payment: The Bigger, The Better

A larger down payment is your superpower as a self-employed borrower. It shows you have skin in the game and reduces the amount you need to borrow. This makes you a much less risky proposition for the lender.

Honestly, if you can swing it, a down payment of 20% or more is fantastic. It not only makes you look good to lenders but also lowers your monthly payments and the total interest you’ll pay over the life of the loan. It’s a win-win situation. If you can't quite manage 20%, even a solid 10% can make a big difference.

Financing Options: Where to Go for Your New Ride

Okay, you’ve got your documents, your credit score is humming along, and you’ve scraped together a decent down payment. Now, where do you actually get the money? There are a few avenues to explore:

1. Dealership Financing: Convenient, But Shop Around!

This is often the easiest route, as you can do everything in one place. Dealerships have relationships with various lenders and can often find you options. However, don't just accept the first offer they throw at you!

Pros: Convenience, sometimes special offers or incentives.

Cons: Rates might not be the absolute best, and they might try to push you into add-ons.

My advice? Pre-approval is key. Get pre-approved for a loan from your bank or a credit union before you even step onto the dealership lot. This gives you leverage and a benchmark to compare against. It’s like going into a negotiation with your homework done. You know your worth!

2. Banks and Credit Unions: Your Trusted Friends

These are generally excellent places to start. Banks and credit unions often offer competitive rates, especially if you’re an existing customer with a good relationship.

Pros: Competitive rates, established institutions, good customer service.

Cons: The application process might feel a bit more traditional and require more upfront paperwork than some online lenders.

Credit unions, in particular, are member-owned and often have a focus on helping their members. It’s worth checking them out, even if you’re not a member yet – sometimes you can join with a small donation to a partner charity. Think of it as a community investment for your new car!

3. Online Lenders: Speed and Simplicity

The online lending space has exploded, and for good reason. Many online lenders specialize in auto loans and offer quick, streamlined application processes. Some are even geared towards borrowers with less-than-perfect credit or those who are self-employed.

Pros: Fast application and approval, often competitive rates, accessible for various credit profiles.

Cons: Can be harder to gauge the reputation of smaller lenders, always read the fine print carefully.

Do your research here! Look for reputable lenders with good reviews. Sites like LendingTree, Credit Karma (they also offer loan comparisons), and others can help you compare offers from multiple lenders at once. It’s like a buffet of loan options!

4. Business Loans (Sometimes!): A Niche Option

For some self-employed individuals, especially those with established businesses and a clear need for the vehicle to be a business asset, a business loan might be an option. This is less common for personal vehicle purchases but worth considering if your car is primarily for your business operations.

Pros: Can potentially offer different terms and interest rates, can keep business and personal finances separate.

Cons: More complex application process, might require more collateral, not suitable for most personal car purchases.

This is a more advanced strategy, so if this is your route, definitely talk to a business advisor or your accountant. It’s not the first stop for most folks buying a car to get to their yoga class, you know?

Pro-Tips for the Savvy Self-Employed Car Buyer

You’re not just buying a car; you’re making a smart business investment that also happens to get you from A to B. So, let’s be strategic.

1. Know Your Numbers, Inside and Out.

This is non-negotiable. Before you even think about test drives, understand your average monthly income, your expenses, and how much you can comfortably afford for a car payment, insurance, and maintenance. Don’t guess. Use your bank statements and tax returns to get a realistic picture.

This isn't about being cheap; it's about being smart. Overextending yourself financially is a quick way to add stress to your already busy life. Nobody wants that!

2. Negotiate, Negotiate, Negotiate!

Whether it’s the car price or the loan terms, never accept the first offer. Do your research on car values, and be prepared to walk away if the deal isn’t right. The same goes for the financing. If a dealership offers you a rate, have your pre-approval from the bank in hand and use it as a bargaining chip.

Remember, they want to sell you a car. You want to buy a car at a good price with affordable financing. It’s a negotiation, not a demand!

3. Read Everything, Then Read It Again.

This goes for loan agreements, financing contracts, and even those pesky warranty offers. Understand all the fees, interest rates (APR!), loan terms, and any penalties for early repayment or late payments. Ignorance is definitely not bliss when it comes to financial contracts.

If something doesn’t make sense, ask questions! Don’t be shy. It’s your money and your financial future on the line. Imagine signing something and then realizing there’s a hidden fee the size of a small country. Yikes!

4. Consider the Total Cost of Ownership.

The sticker price of the car is just the beginning. Think about insurance costs (especially if you’re driving a brand-new luxury SUV for your freelance pottery business!), fuel efficiency, maintenance, and potential repair costs. A cheaper car upfront might cost you more in the long run if it’s a gas guzzler or prone to breakdowns.

It’s like choosing between a budget-friendly coffee maker and that fancy espresso machine again. Sometimes the initial investment pays off in quality and long-term savings. Or, you know, in better-tasting coffee for your workday.

The Takeaway: You Got This!

Financing a car as a self-employed individual might require a bit more preparation and strategic thinking, but it is absolutely achievable. The key is to be organized, transparent, and to shop around for the best deal. You’re already proving your ability to manage your own business, so managing your car financing is just another skill you can master.

So, take a deep breath, gather your documents, and get ready to drive away in a car that makes you feel confident and capable. You’re building your own success story, and sometimes, that story needs a reliable set of wheels. Now go get ‘em!